China's Green Leap Forward

- Jonathan Wilmot

- Jan 26, 2024

- 3 min read

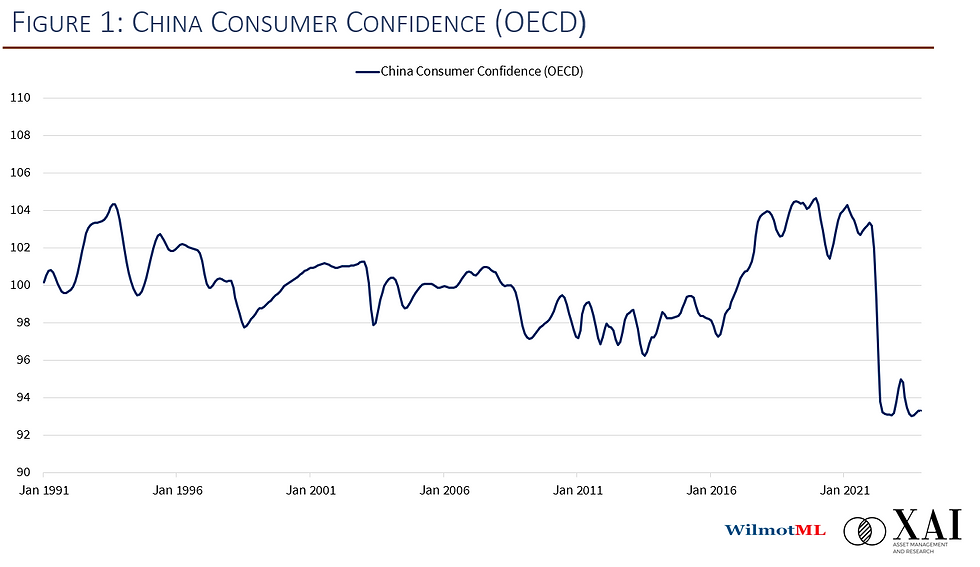

China is not a happy place right now. Business and consumer confidence have been crushed underfoot by President Xi’s brutal COVID lockdowns and ruthless approach to rival sources of power within the party – and even more so from the private sector; the population has begun to shrink, (low birthrate); youth unemployment is high and rising and many of the younger generation see little exciting or hopeful in their futures. Unlike Russia the country hasn’t yet regressed into a stagnant Stalinist ( or late-Mao type) dystopia, but politically that seems to be the risk inherent in Xi's personality cult.

Markets don’t like it. Domestic capital is trying to leave, foreign capital is no longer flowing in and the chronic net capital inflow of the 2000s has been replaced by a chronic capital outflow. Over the past year, MSCI China is down 32% percent versus plus 20% percent for the S&P 500; since the COVID low of March 2020, US equities are up about 125%, and Chinese equities are down around 30%.

And yet...... China has achieved something over the past year which arguably dwarfs anything else achieved in the world economy in recent years, and moreover has huge implications for the planet and the future of geo-politics.

Their Green Leap Forward in 2023 is absolutely stunning - as summarised in the charts below and more fully documented here by Carbon Brief. Whether you look at industrial production (Figure 2), investment, or contribution to GDP, green technologies (solar panels, electric vehicles, batteries, wind turbines, pumped hydro storage) have become the main drivers of growth. Computer chips, robotics and to some extent AI have also been booming. So as the old economy (real estate, fossil fuels especially) go into a managed decline, the new economy is set to explode up the S-curve.

Source: Carbon Brief

In 2023 alone, China installed some 200 GW of new solar and wind capacity, double last year's total and four times the average in the three years before COVID. (it is also twice as much as the UK's entire electricity production capacity). Production of EVs rose 30% last year while investment in EV production and charging infrastructure rose by a similar amount. (EVs now comprise almost a third of vehicle production and domestic sales). In total, investment in clean energy sectors rose some 40%y/y in 2023, accounting for more that 100% of Chinese investment growth.

Of course, the Achilles heel of solar and wind is their intermittency: the sun doesn't always shine, and the wind doesn't always blow. But China's investment in storage capacity has also surged, allowing clean electricity supply to be distributed more effectively. There was almost 170GW of pumped hydro storage capacity under construction at the end of 2023, compared to 120GW under construction a year earlier. Figure 4 shows the scale and breadth of the effort to team up intermittent supply with hydro storage capacity.

Source: Carbon Brief

Meanwhile, prices of solar panels dropped by 40%, and EV battery units by 50% last year. Domestic overcapacity looms, and as a result the rest of the world is bracing for an onslaught of cheap Chinese, EVs, batteries, solar panels and wind turbines - not to mention many of the components needed for full electrification.

Why this matters...

1) Chinese electricity consumption is equivalent to the US and EU combined: unless China decarbonises rapidly the world has absolutely no chance of achieving its climate targets.

2) In 2022, renewables and nuclear accounted for only 1/3rd of domestic electricity supply, in China with coal a big share of the balance. (That compares with 60.8% in Europe and 40.6% in the US and the UK with coal capacity pretty small).

3) Full electrification including most of the transport sector will probably require 10-30% more generation capacity than we have currently in most countries, so it's likely that investment in clean energy supply, infrastructure and vehicles will be continue to be a big driver of growth for several years to come.

4) By subsidising and promoting clean energy investments China is helping to speed up the technology learning process, and the drop in the cost of clean energy and EVs for everyone (good news for Chinese consumers and the entire planet - but bound to be a new flashpoint for protectionist thinking in the West).

More on the implications shortly.

Commentaires