November CPI: Gradual Disinflationary Progress Tempered by Rising Goods Pressures

- Alex Haseldine

- Dec 12, 2024

- 2 min read

Yesterday's November CPI report indicates that underlying inflation is making steady, if unspectacular, progress towards 2%, but highlights risks from the goods sector. Headline CPI rose 0.3% month-over-month, an increase from October’s 0.2% gain, while core CPI advanced 0.3% for the third consecutive month.

The most notable development this month is the renewed upward momentum in core goods inflation. November’s 0.3% gain follows a 0.2% increase in October and a flat reading in September. Within this category, used vehicles rose 2% on the month, and 5% over the past three months. This trend suggests a possible repricing in anticipation of cost pressures related to potential future tariffs. CPI goods inflation now appears to be converging with upstream indicators such as the Producer Price Index (PPI). Today's Producer Price Index (PPI) release will be important for gauging the extent of any tariff-related cost pass-through, as evidence of firms “pre-charging” for potential tariff costs would complicate the FOMC’s efforts to guide inflation back to 2%.

Policy communications from Fed officials, including Chair Powell and Governor Waller, have recently indicated a cautious approach to policy easing amid persistent uncertainties. The risk of tariff-driven cost pass-through elevates the hurdle for sustained rate reductions next year, particularly if these pressures gain traction and broaden beyond the automotive and related segments.

On a more encouraging note, services inflation remains stable to slightly slower. Core services posted a 0.3% rise, showing some moderation in momentum. Crucially, any material divergence in goods prices will demand clearer disinflation in services if the Federal Open Market Committee (FOMC) is to justify continued easing toward a more neutral stance. Indeed, recent communications by FOMC members, such as New York Fed President Williams, have emphasized data dependence in navigating from a restrictive setting. Stabilizing services inflation, alongside cooling measures of underlying price pressures in certain subcategories, suggests the economy may still be on track for further disinflation, albeit gradually.

Another 25 basis point cut at the upcoming December meeting is still in play, Without clearer evidence of sustained moderation in services prices, and if goods inflation is indeed being propped up by anticipated trade barriers, the FOMC will find it increasingly challenging to justify multiple cuts next year. In this context, market expectations have shifted only slightly in response to the latest data. The CME Group’s FedWatch tool now places a 55.2% probability on a 25bp cut in March 2025 and a 61.5% chance of another cut by mid-2025—down marginally from 62.2% last week.

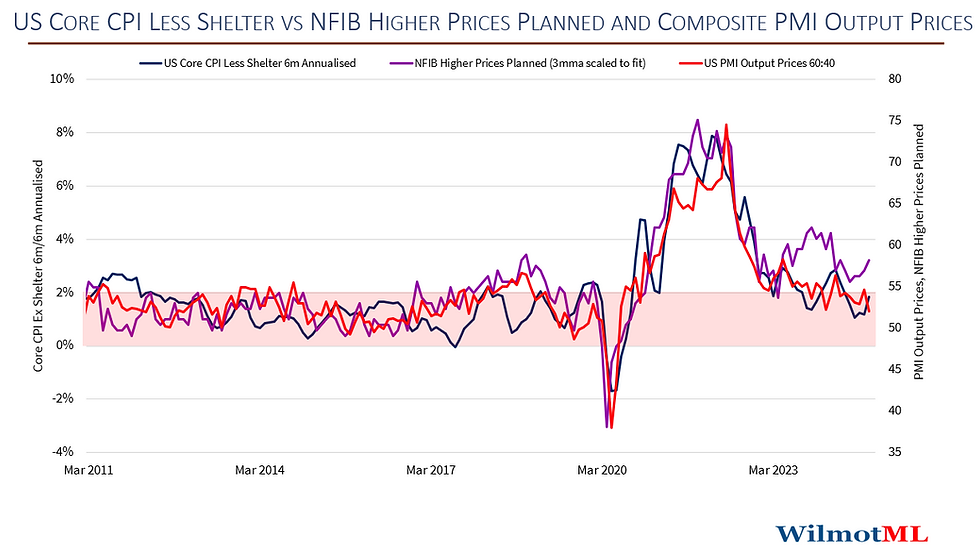

Some charts below:

コメント