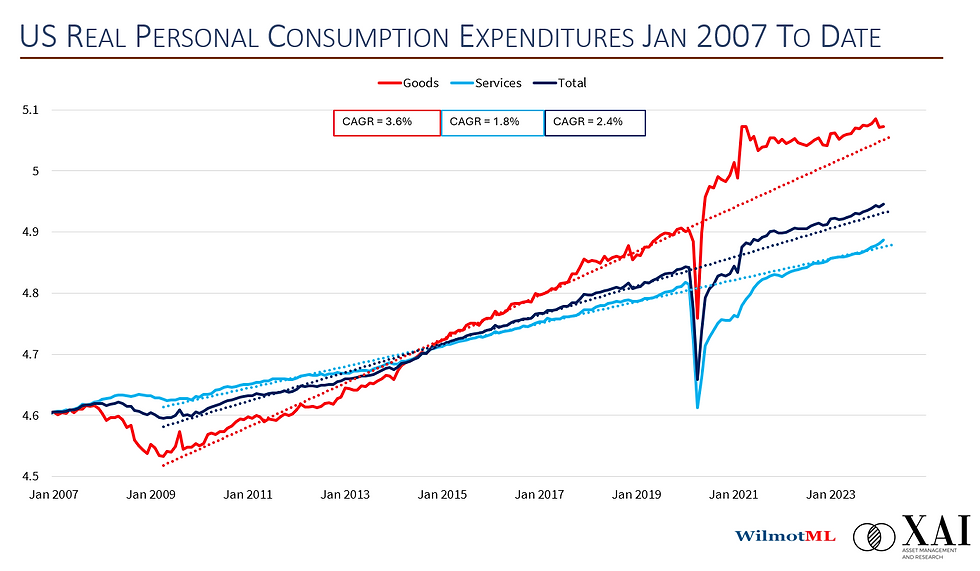

Another strong payrolls report for March means that private employment growth ticked higher in Q1:2024. For the latest quarter private payrolls were growing at 1.8% per annum versus 1.4% in Q4:2023. The most recent peak was 6.5% per annum in Q4:2021 -figure 1. . Our favourite indicator of underlying inflation pressure also picked up in March - figure 2. Real personal consumption spending in February remains solidly on its post-COVID trend (of 3.6% pa), with faster services spending growth taking the lead over the last two months.

All of this data has effectively come out since just before last Fed meeting: none of it supports early rate cuts. But should we expect more of the same in Q2?

Probably not: our guess is we are more likely to get a resumption of the cooling trend in employment growth and inflation than a repeat of Q1. Nonetheless, GDP growth looks to have stabilised in the 2-2.5% peer annum range and it will take some better than expected (core) inflation numbers this week to revive hopes of rate cuts any time soon.

Comments